Tourism: Arrivals remain the same, but we are heading for record revenues thanks to Americ

Source: ProtoThema English

With the arrival of September, the “hot” two months of summer close, in a season with quite a few ups and downs and an asymmetrical picture across destinations in Greece.

And if, at the peak of Greek tourism in the heart of summer, there were no shortage of complaints from destinations about tourists who do come but spend less, the first forecast now regarding how tourism revenues will ultimately shape up this year tips the scale even toward an increase compared to 2024, the year in which the historic record of €21.6 billion was achieved, including cruise revenues.

The strong performance of the American market this year—recording impressive numbers in arrivals and revenues, even against other European markets—as well as the continuing positive course of key European markets are two basic “pluses” for the industry this summer.

In addition, inflation—with rising prices in the tourism “package” across destinations—the decrease in the share of road arrivals from nearby markets that spend less in Greece (which in previous years pushed average spending down), and the increase in scheduled airline seats (note: 7 out of 10 foreign visitors come by air) this autumn, not only compared to last year but even higher than July–August 2025, are three more factors that seem able to lead to higher spending numbers and thus higher total revenues for Greek tourism this year.

In general, regarding inbound traffic, the picture is more fluid, something reflected in official numbers, since already in the first half of 2025 there is only a marginal increase of 0.6%, with even a drop in June of 1.7%, according to the Bank of Greece’s travel balance data. Tourism officials do not rule out a decline for the first time, despite the contradiction that international air arrivals rose in both June (+5.4%) and July (+4.6%) compared to the same months of last year.

Even so, in this case, the Cyclades, due to Santorini, are the only geographical unit in Greece recording a decline this year of -7.4% in international air arrivals in the seven-month period, at levels just below 638,000, with the drop in July at -2.8% with 319,000 international air arrivals.

The critical third quarter

The… unofficial, fluid picture is seen especially in the most critical period of high season, July–August: this year signals remain mixed, with the industry eagerly awaiting their reflection in the Bank of Greece’s official figures.

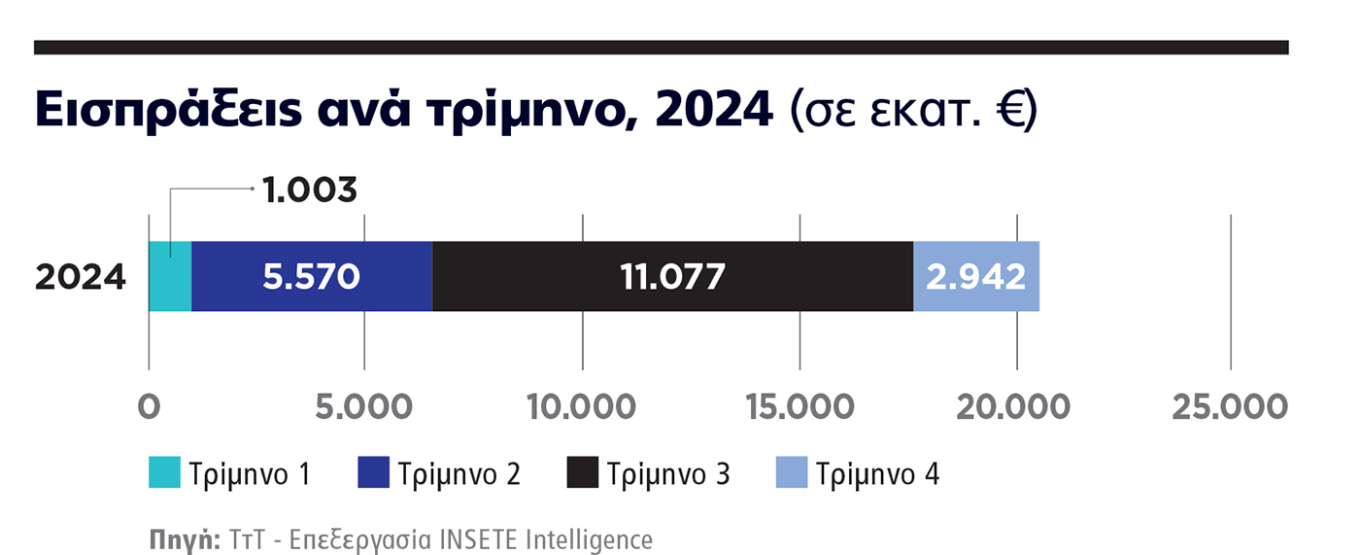

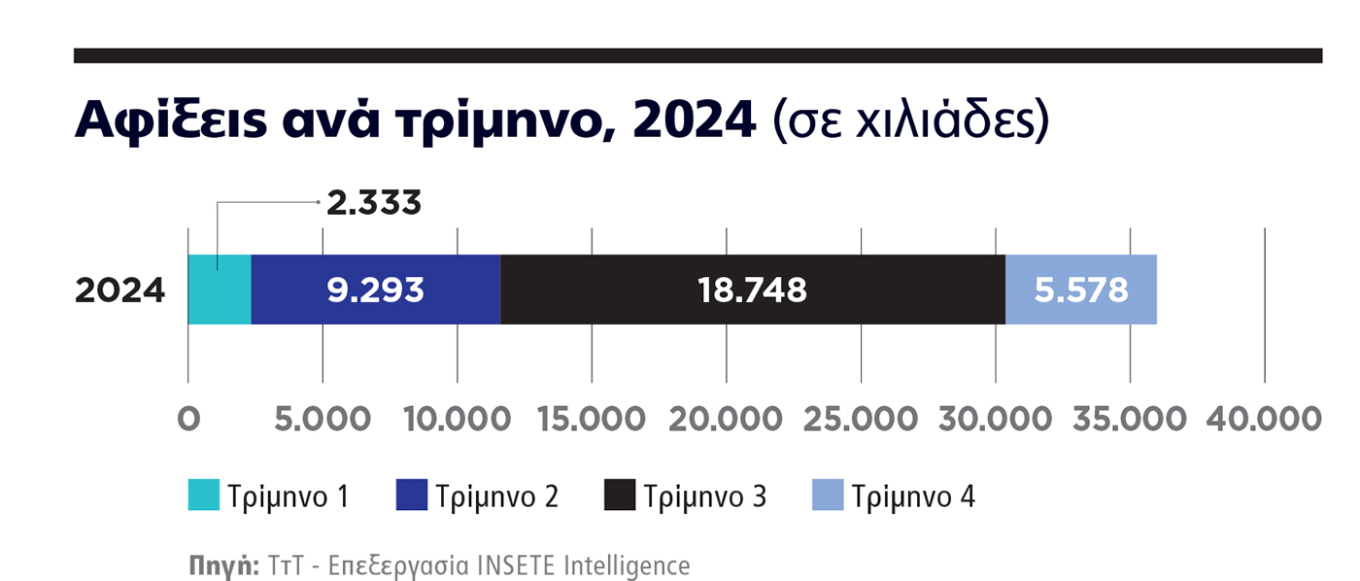

It should be noted that the third quarter traditionally determines, to the greatest extent, the figures of Greek tourism, since July–August account for more than half of total tourism revenues each year. Specifically, based on last year’s numbers, 54% of the total (from nearly 60% in 2019), while in terms of arrivals the figure was 52% last year (56% in 2019).

In more concrete numbers: out of a total of €20.59 billion in revenues (excluding cruises, with which last year’s revenues rose to €21.6 billion), the July–August period corresponds to €11.077 billion, while out of 35.95 million arrivals (excluding cruises, with which arrivals rise to 40.7 million travelers), Q3 arrivals reached 18.75 million.

Even though in 2024 seasonality figures were somewhat softened—and with a similar trend this year—the “Sun and Sea” product still plays a decisive role for the industry’s performance. At the start of this summer, Bank of Greece data already for June 2025 suggest that arrivals are gradually hitting a “ceiling” for summer, with revenues performing positively.

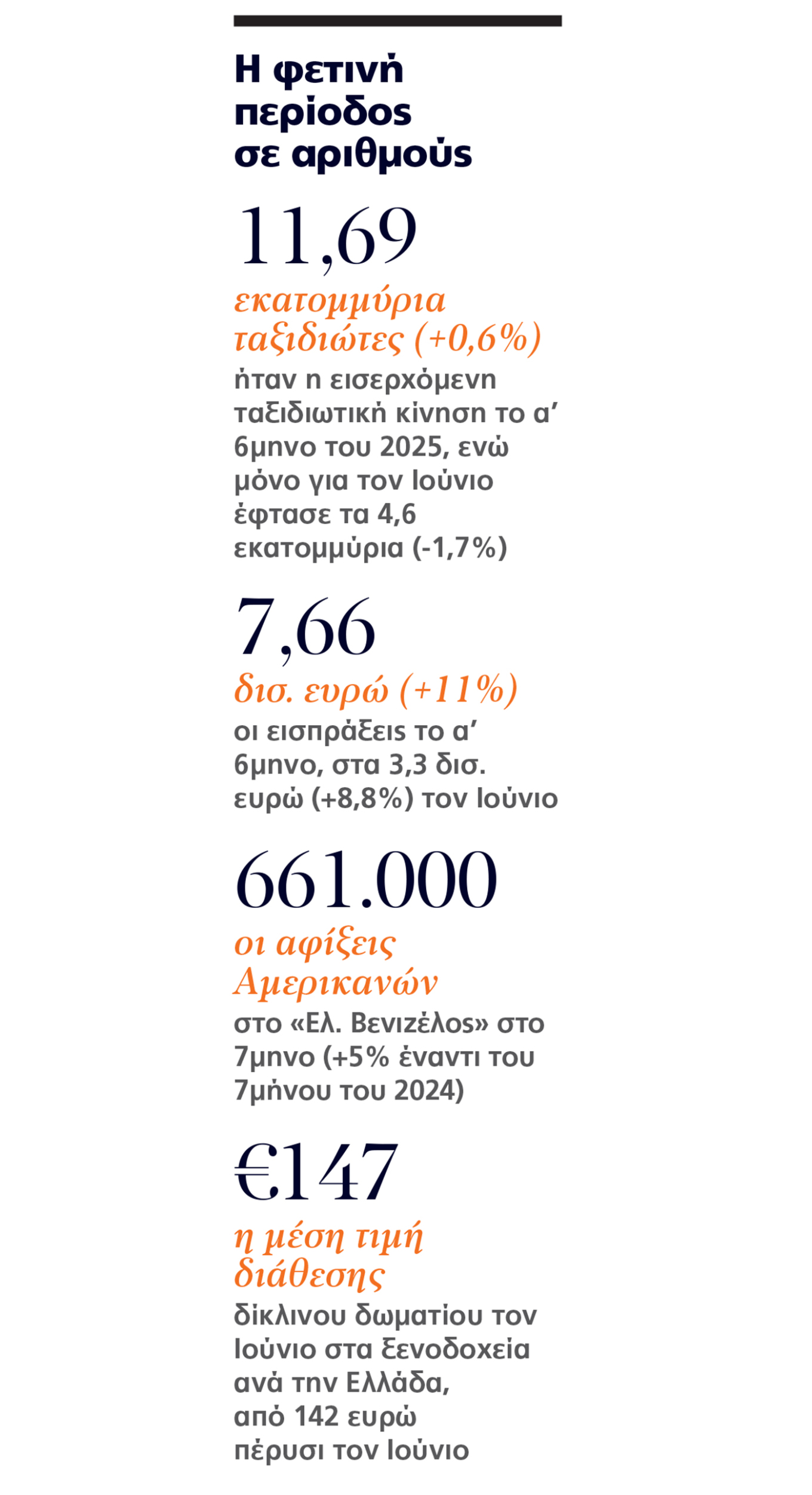

June closed with a 1.7% decline in inbound travel, at 4.6 million travelers, and an 8.8% increase in revenues to €3.3 billion, while in the first half of the year travel movement stood at 11.69 million with a marginal rise of 0.6% and revenues at €7.66 billion, with double-digit growth of 11%.

Including July, for now the only official data come from airports, where numbers are again positive, with a 4.7% increase in total passenger traffic (domestic–international, arrivals–departures) in January–July 2025, reaching 44.73 million travelers.

Of particular interest are the figures for international air arrivals, where the latest INSETE data show a 5.3% increase in the January–July seven-month period, with a total of 15.2 million travelers, i.e., 769,000 more compared to the same period in 2024. Only in July, according to INSETE, there were 4.9 million arrivals, up by 212,000 travelers or +4.6% compared to July 2024.

The 5 key parameters

In a first review of this summer season, there are five key factors that seem likely to largely determine the course of revenues for tourism in 2025:

• Increase in airline seats during autumn: Since last year there has been a significant increase in scheduled seats by both Greek and foreign airlines in autumn, due to the trend of more Europeans traveling outside peak season, to avoid both heat and especially high August prices.

This trend is recorded this year too, in Greece and other major Mediterranean markets. For Greece, according to INSETE data, both for September (over 943,000 seats) and October (over 583,000), the increase in scheduled airline seats to Greek destinations stands at +4.9% for both months, compared to +3.4% in July and +4.3% in August.

• The strong performance of the American market: This summer the US market has more flights than ever—103 weekly—and already in the first half has recorded the highest growth among Greece’s top 5 foreign markets (Germany, UK, France, Italy, USA). Furthermore, for May 2026, a new destination—Dallas—has been announced and has been in booking systems since August 11.

At Athens International Airport, American resident arrivals in the seven-month period reached 661,000, up 5% from 629,000 in the same period of 2024. July alone recorded a 5% increase. At the same time, Bank of Greece data show that revenues from the US exceeded €700 million for the first time in the first half of 2025, with €247 million in June alone. The January–June 2025 revenue increase corresponds to +29.4%, reaching €704 million compared to €544 million in 2024, while June alone saw an impressive +65% increase, at €247 million.

This year, Greece stands out by raising its numbers in double digits compared to inbound traffic from the US. Apart from Greece’s growing profile in the US, boosted by increased air connections (over 100 weekly flights for the first time this summer), the Greek diaspora also plays a very important role.

• The performance of other key markets: Even if some core inbound markets already show declines in arrivals in H1 (e.g., France -9.8% in January–June), revenues are up across all, likely due to higher prices. Even France shows a +2.1% revenue rise.

Germany is running at double-digit revenue growth of 13.5%, with arrivals up 4.7%. UK travelers are more conservative, with lower average spending (+11% arrivals, +7% revenues in H1; June arrivals +14.9% but revenues only +3%). Though smaller in share, Israel’s data are also interesting.

Contrary to initial June estimates when the geopolitical crisis broke out, Greece this summer shows further growth. At Athens Airport, Israeli arrivals in January–July 2025 rose by an impressive 51% to 202,000, compared to 134,000 in the same period of 2024. July alone saw about 31,000 Israeli arrivals.

Double-digit growth is also recorded at the 14 regional airports under Fraport Greece. Despite market difficulties early this summer, passenger traffic from/to Israel rose by 12.6%, with 17,000 more passengers compared to July 2024.

• Inflation and prices: According to Eurostat, Greece’s annual inflation stood at 3.7% in July, after 3.6% in June, and 3% in July 2024. Eurozone inflation remained at 2% in July 2025, unchanged from June, compared to 2.6% a year earlier. As for hotel prices, according to ITEP (Institute for Tourism Research and Forecasts of the Hellenic Chamber of Hotels), the average rate for a double room in June 2025 across Greece was €147, compared to €142 last year.

• A “hidden” factor: fewer road arrivals: Bank of Greece data show a sharp June drop in revenues and inbound travel from non-euro EU countries, which include key road-tourism markets for Greece like Bulgaria and Romania.

The June revenue drop from non-euro countries was 18.8%, while inbound traffic plunged 35.5%, suggesting Greece has become more expensive for nearby markets coming by car.

Road arrivals, which mainly feed Northern Greece’s tourism, were what dragged average spending down in previous years because Balkan tourists spend less. Now, in H1 2025, average spending per trip stands at €623, up 10.1% compared to 2024; in June alone, it exceeded €682, up 10.2%.

Ask me anything

Explore related questions

The original article: belongs to ProtoThema English .